The Alpha and Omega of Regulation (via Omicron)?

Having said goodbye to another year of headlines dominated by COVID-19, with a Christmas and New Year overshadowed by a mixture of good and bad news about Omicron, it's not yet clear what degree of optimism about the year ahead is justified. At the very least, it is to be hoped that the World Health Organisation will not find it has to exhaust the Greek alphabet in naming any future new variants of concern. Despite the seemingly interminable global health crisis, however, the pace of change in the financial services industry has not slowed. If anything, there are even more changes and innovations than ever before: the coming year is arguably unprecedented in terms of the sheer volume of weighty developments.

And now that the UK is a year on from the end of the Brexit transition period, there is barely any talk these days about seeking "equivalence" with the EU; the focus is now on "divergence" and "deference". Indeed, if there is one theme that applies across all those regimes which the UK has "inherited" from the EU – and in relation to new ones going forward – it is the extent to which the UK is diverging from the bloc in reformulating UK regulation. Many things may, on the surface, look quite similar in terms of the supervisory preoccupations – but the detailed and practical application may end up being very different.

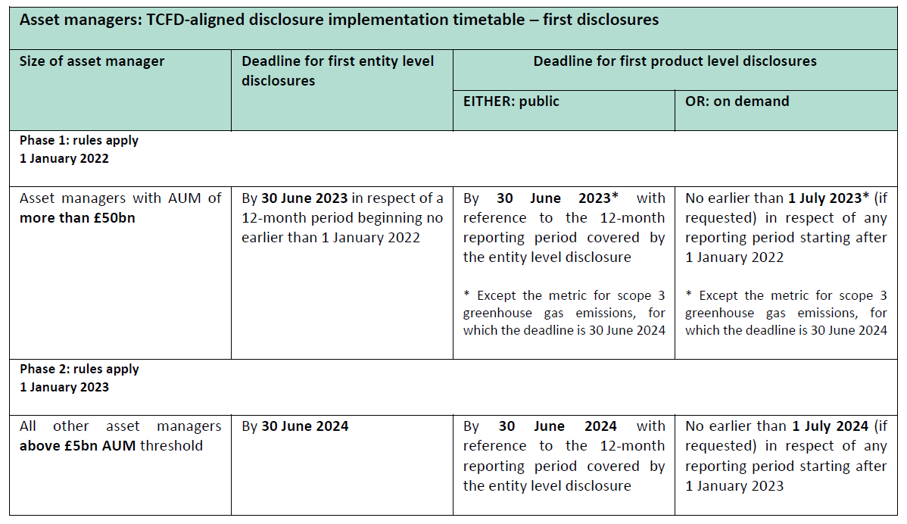

Climate change and sustainability remains close to the top – if not at the top – of the agenda for many firms. The UK sustainability regime for asset managers and owners is starting to take shape: TCFD-aligned disclosure rules, both at the entity and product levels, are now in force for the largest asset managers and will apply to others from next year. High level proposals for a Sustainability Disclosure Regime that will "overlay" those rules which emerged towards the end of last year and will evolve and become more concrete through the course of 2022 and beyond, as will the UK Green Taxonomy. By contrast, the EU regime is more evolved in terms of application and detail, though even then delays to technical standards have contributed to considerable uncertainty. To a greater or lesser extent, divergence between the UK and EU seems inevitable. See Part 1: ESG and Sustainability.

As regards prudential regulation, the UK's Investment Firm Prudential Regime went live on New Year's Day: as with other large regulatory change projects of course, while there was much to be done by the implementation deadline, work did not stop then. Adjusting to the new regime as it beds down will present ongoing challenges for the regulator and the regulated alike. At the same time, UK banks became subject to a set of new rules implementing most of the Basel III recommendations – but there will be still more to come under "Basel 3.1". EU banks are subject to the same recommendations, implemented via the Capital Requirements Regulation. Private equity and venture capital firms have a vested interest in how a section of these UK and EU rules are implemented and applied since they affect how banks must assign risk weights to private equity investments. Similar rules (in concept at least) may apply to insurance companies under the UK and EU versions of the Solvency II regime. See Part 2: Prudential regulation.

While the UK and EU share many of the same concerns when it comes to the regulation of investment funds, divergent approaches in terms of how to address them are already clear in terms of the granular detail . For instance, in relation to PRIIPs, the FCA has expressed quite trenchant views about what it sees as dysfunctional aspects of the regime and is changing its rules and guidance, as well as the 'onshored' technical standards; the EU is also changing its version of the PRIIPs RTS, together with a modest extension to the "PRIIPs exemption" for UCITS managers. The UK has finished the statutory framework for its new Overseas Funds Regime which will enable non-UK retail funds (including EEA UCITS) to access the UK retail market, subject to an assessment of equivalence and recognition – the FCA will now be consulting on the rules to facilitate the regime. And the UK's new regime for Long-Term Asset Funds (LTAFs) is now in force – it remains to be seen whether and how this takes off. In terms of alternative funds, the EU has set the legislative ball rolling with its proposed directive on changes to EU AIFMD (and EU UCITS Directive) (the so-called "AIFMD II" review). This will not come into force until 2024 at the earliest. However, the EU Cross Border Distribution of Funds regime is now up and running and will impact on marketing and pre-marketing of funds in the EU. None of this will apply in the UK, but UK and other non-EU managers seeking to market AIFs may be impacted by amendments to the NPPR regimes of individual Member States. See Part 3: Investment funds.

The UK and EU MiFID II "ships" continue to sail in broadly the same general direction, but already there are discernible changes of course. Among other things, the UK has ditched the requirements for best execution reports, and proposes to remove the share trading obligation and double volume cap restrictions. Changes to the UK research and inducements rules take place in March. The EU is also planning amendments to the EU MiFID II regime, but by and large, none of the changes correlate with one another. See Part 4: MiFID II.

In terms of governance and outsourcing, the UK regulators are - not surprisingly after the last couple of years we have had - heavily focused on the operational resilience of FCA-authorised firms, banks, insurers and FMIs. They are also seeking to embed and enhance diversity and inclusion into the way that all financial services firms work and structure themselves. In the UK, EU and globally, outsourcing – and particularly outsourcing to the cloud – remains a consistent preoccupation of the supervisors. See Part 5: Governance and Outsourcing.

When it comes to AML/CTF both the UK and EU are proposing changes to their regimes. There will be changes to the UK Money Laundering Regulations and – after threatening it for some time – the EU will be negotiating a new, directly-applicable Regulation on AML/CFT and a Sixth Money Laundering Directive (MLD 6). Meanwhile, UK firms above a certain size will find themselves subject to the new economic crime levy, to be assessed in a levy year starting on 1 April 2022 and payable next year. See Part 6: Financial crime.

It has been an exciting year in the world of fintech, which began with the Kalifa Fintech Review highlighting the opportunity to create highly skilled jobs across the UK, boost trade, and extend the UK's competitive edge over other leading fintech hubs. The UK is continuing its exploratory and consultative work on digital assets and stablecoins, and the development of Central Bank Digital Currency, while the EU is pursuing the various legislative initiatives under its Digital Finance Strategy. These developments will impact on financial market infrastructures, payment institutions, other fintech firms and, ultimately, with the launch of digital money, businesses and households. See Part 7: Fintech.

The UK and EU are each reviewing their respective "versions" of the Securitisation Regulation – the UK will be pursuing its now familiar approach of making "targeted amendments" to tailor the regime for the UK market. Again, in terms of overall substance, the regimes will likely end up looking very similar to one another, but the detailed application may differ quite significantly. The EU Credit Servicers and Credit Purchasers Directive is now finalised and it is now up to EU Member States to transpose the measures into national law and apply them from 30 December 2023. The UK is not planning an analogous regime though UK firms which advise or manage funds investing in EU secondary credit will be indirectly affected by the EU changes. See Part 8: Markets and trading.

Financial markets infrastructure continues to be the focus of much attention on both sides of the English Channel (or, depending on your perspective, La Manche). The European Commission continues to express its dissatisfaction with the over-reliance in the EU on UK CCPs for some derivatives clearing activities. The time-limited equivalence decision for UK CCPs – originally designed to avoid a financial stability "cliff edge" – is due to expire on 30 June 2022. Mairead McGuinness, Commissioner for Financial Services, Financial Stability and Capital Markets Union has said she will be recommending an extension to that equivalence decision shortly – but only long enough for the EU supervisory system for CCPs to be revised to reduce the over-reliance on the UK. Aside from that, the EU CCP Recovery and Resolution Regime will largely kick in on 12 August 2022 while the Treasury has consulted on expanding the existing Banking Act resolution regime for UK CCPs. The Treasury also seems set on creating a version of the Senior Managers & Certification Regime (SMCR) for CCPs and other FMIs. The UK Payments Landscape Review is continuing and the Payment Systems Regulator has set out its policy statement on the New Payments Architecture; meanwhile, a review of the EU Payment Services Directive is coming. The mandatory buy-in framework under the EU settlement discipline regime has been postponed yet again (although we understand the cash penalty regime will come into force as scheduled on 1 February 2022), and beyond that we may be seeing a "CSDR REFIT" in the not-too-distant future as a result of the findings of the review of the EU Central Securities Depositories Regulation. See Part 9: Financial market infrastructure.

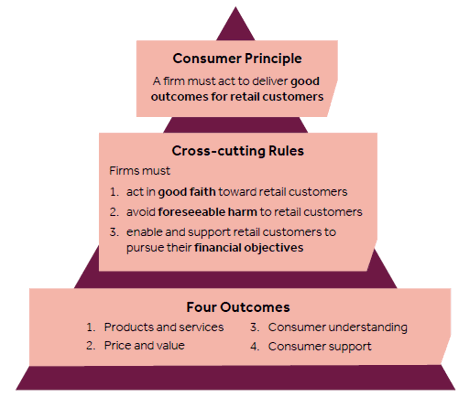

Finally – and perhaps most fundamentally for UK firms and the overall shape of UK financial services regulation in the future – reforms arising out of the Financial Services Future Regulatory Framework Review will usher in a more regulator-led approach to rulemaking, with swathes of EU-derived legislation moving off the statute book and into rulebooks. While there will no doubt be complications, at the "coal face" it may at least be easier to find and navigate the applicable rules. The government has said its general intention is to amend, replace or repeal retained EU law "that is not right for the UK" and will be issuing proposals in Spring 2022. In looking at non-UK firms seeking access to the UK market, there will be an increasing use of regulatory deference, an international concept intended to be less hidebound and codified than the EU concept of equivalence. Less holistically, the Treasury is conducting a Wholesale Markets Review intended to untie some of the restrictions imposed on the wholesale secondary markets by the inherited MiFID II regime; in the retail sector, the FCA has proposed a significant new Consumer Duty which is looking like it may turn out to be a resource-heavy regulatory change project on a tight timetable for many firms that service that sector. That, together with the FCA's proposals for improving the UK appointed representatives regime and the financial promotions regime mean that, at the domestic level alone, there is much to do. And, against that backdrop, firms should expect the FCA to be a tougher, more proactive and more intrusive supervisor: led by Nikhil Rathi as Chief Executive, it has committed to being "more innovative, assertive and adaptive" and this is certainly consistent with our confidential experience of the way in which the regulator is already dealing with many of the firms it regulates. As an example of this new approach, in December 2021, the FCA confirmed changes to its internal supervisory and enforcement process that will mean that many (but not all) decisions to issue statutory notices against firms or individuals will no longer be made by the Regulatory Decisions Committee but will be made by individual FCA staff members under the regulator's Executive Procedures instead – decision-making will be faster without, the FCA says, compromising the rights and protections of firms and individuals. See Part 10: UK financial services regulation.

So 2022 will be busier, more complicated and more challenging than ever, with firms having to face and adapt to the many changes affecting the industry, all against a backdrop of continuing global uncertainty. This time last year, after a Christmas in lockdown, we quoted the wartime leader Winston Churchill. This year, with the news see-sawing between the concerning and the encouraging, it seems fitting to quote him again:

"I am an optimist. It does not seem too much use being anything else."